: Is The 12.4% Yield From Cannabis Credit Investable?")

Pipat Yapathanasap/iStock via Getty Images

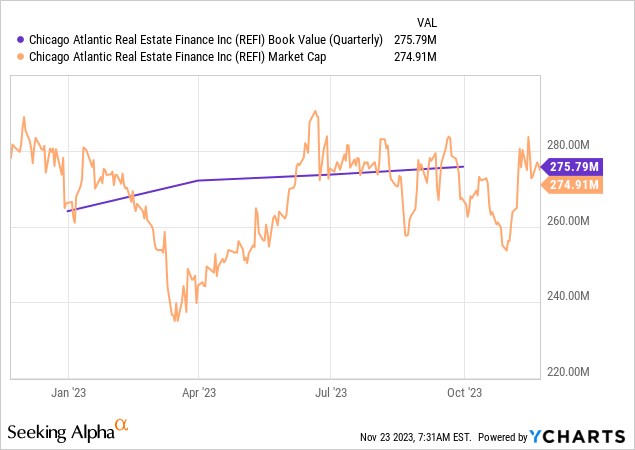

Chicago Atlantic Real Estate Finance (NASDAQ:REFI) is the slightly larger cannabis mortgage REIT versus peer AFC Gamma (AFCG). Its focus on cannabis credit has meant a multi-layered risk profile from both rising interest rates over the last 2 years and concentration in a single industry that has seen intense headwinds to profitability and liquidity. The fat yield is the prize against common shares that are flat year-to-date with REFI last paying out a $0.47 per share quarterly distribution for a 12.4% annualized dividend yield. This was unchanged from its prior distribution and came with the common shares essentially trading at par with a book value of $275 million, around $15.17 per share. Diversification and risk management are crucial against a sector that’s realized a broad deterioration of liquidity and faces continued near-term legislative uncertainty. I last covered REFI back in May and a reevaluation of its financials from the latest earnings and against a set-to-change macroeconomic backdrop is needed.

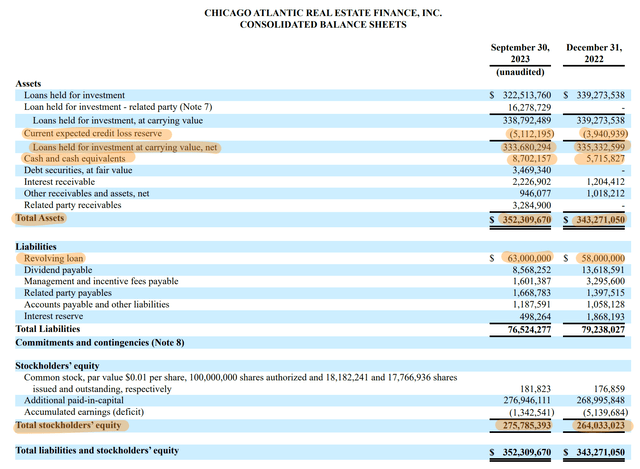

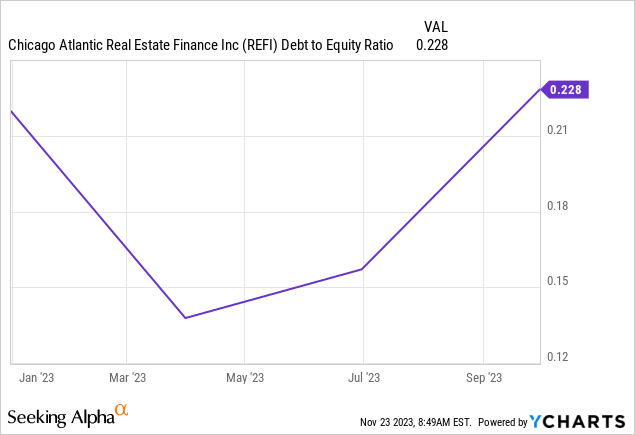

REFI’s credit portfolio was valued at $333.7 million at the end of its last reported fiscal 2023 third quarter after adjusting for a current expected credit loss reserve of $5.1 million. CECL reserve was up 30% from the end of 2022 to drive a broad decline in its credit portfolio of around $1.65 million. The mREIT has built a balance sheet more on equity with a total debt of just $63 million at the end of the third quarter. This meant a debt-to-equity ratio of just 0.22x, an incredibly low base, and one of the lowest debt-to-equity ratios of any mortgage REIT.

Chicago Atlantic Real Estate Finance Fiscal 2023 Third Quarter Form 10-Q

Debt-To-Equity, Commitments, And Risk

Whilst REFI’s debt-to-equity ratio has been on the rise, the current ratio is materially below the conventional 1x watermark of comfort. The externally managed mREIT has been prudent in its use of leverage through a heavy equity layer which has fundamentally rendered the commons safer. This infers lower volatility for the dividend as REFI could lean on debt to meet any future shortfalls in a scenario where there is a level of disruption to interest income.

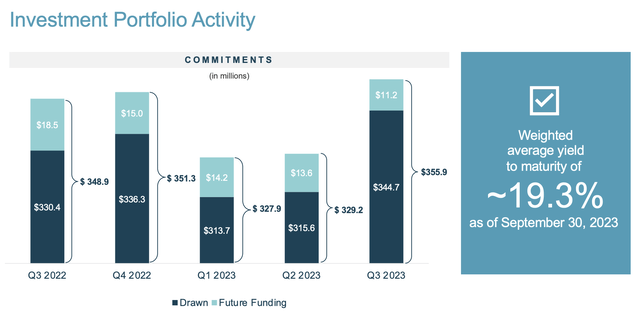

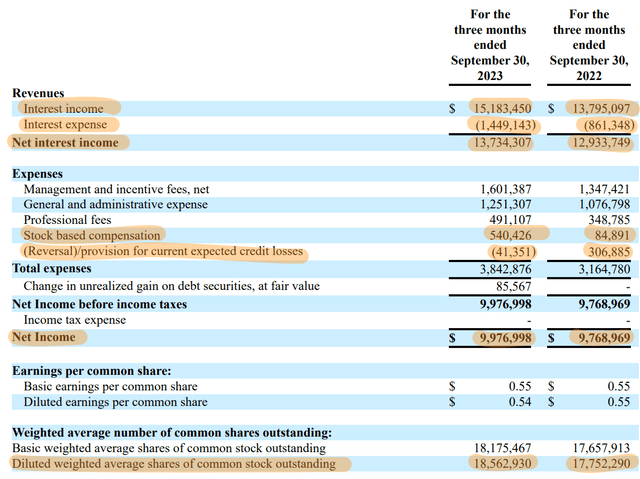

REFI reported third-quarter net interest income of $13.73 million, up 6.2% over its year-ago comp but a miss by $510,00 on consensus estimates. This was driven by total loan commitments of $355.9 million across 27 portfolio investments with roughly $11.2 million of this figure set for future fundings. REFI credit portfolio came with a weighted average yield to maturity of 19.3% at the end of the third quarter, up 10 basis points sequentially. This yield is outsized due to cannabis being classified as a Schedule I drug to broadly restrict the supply of credit. Hence, there is less competition in REFI’s loan origination pipeline which stood at $640 million at the end of the third quarter.

Chicago Atlantic Real Estate Finance Fiscal 2023 Third Quarter Supplemental

This forms a critical reason for buying REFI over other mREITs. US cannabis sales, adult-use and medical, are set to come in at $33.6 billion for 2023 with expectations of growth to $56.9 billion by 2028. This is a large and growing market that needs capital to grow. The inverse also forms a core risk for REFI as its tenants. To be clear, less competition is great for REFI’s yield but also not great for the industry’s ability to have constant and expanded access to capital required for healthy balance sheets and long-term viability.

Operations, Diversification, And Dividend Coverage

Chicago Atlantic Real Estate Finance Fiscal 2023 Third Quarter Supplemental

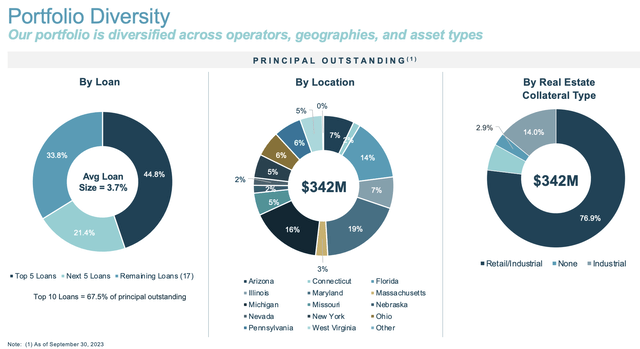

REFI is somewhat diversified but with its top 5 loans constituting 44.8% of its principal and its top 10 loans accounting for 67.5% of its principal. The top 5 concentration is beyond my point of comfort even with REFI diversified across several states and with around 77% of collateral against its loans from retail cannabis property. The REIT has placed its real estate collateral coverage at 1.5x at the end of the third quarter, unchanged sequentially.

Chicago Atlantic Real Estate Finance Fiscal 2023 Third Quarter Form 10-Q

Net income at $9.98 million meant diluted earnings per share of $0.54, down 1 cent over REFI’s year-ago comp. This came as the mREIT realized total gross originations of $35.4 million with around $32.8 million of this funding to new borrowers. Repayments of $10.9 million meant net originations of $24.5 million during the third quarter. The mREIT also has roughly $25 million in liquidity on the back of its revolving credit facility. EPS currently means REFI is covering its dividend by 115%, around an 87% payout ratio. Hence, whilst the somewhat heavy concentration of just five borrowers could present a near-term headwind if credit conditions deteriorate for cannabis companies, REFI is confidently covering its dividend. The ticker is a hold on the back of its low leverage and high yield on debt.