Stock: Reinvesting My Dividends Continue On The Horizon")

Vito Palmisano/iStock via Getty Images

Thesis

In this article, I want to discuss why I continue to add Horizon Technology Finance (NASDAQ:HRZN) to the Business Development Company (BDC) portion of my investment portfolio. I believe their unique exposure in life science & technology, demonstrated financial stability, and commitment to dividends, support it being a long-term income investment play.

Strategy & Performance

Horizon Technology Finance is a BDC operating as a venture lending platform which specializes in offering structured debt products to life science and technology companies. They design financing solutions to support business and development plans. Horizon’s flexible growth-oriented loans, with transaction sizes up to $50 million, cover various industries: technology, life science, healthcare information, and sustainability. The main structure of equity and unsecured debt, with terms of 3-5 years, makes Horizon a strategic partner for companies seeking to gain equity funding with less dilution to their capital.

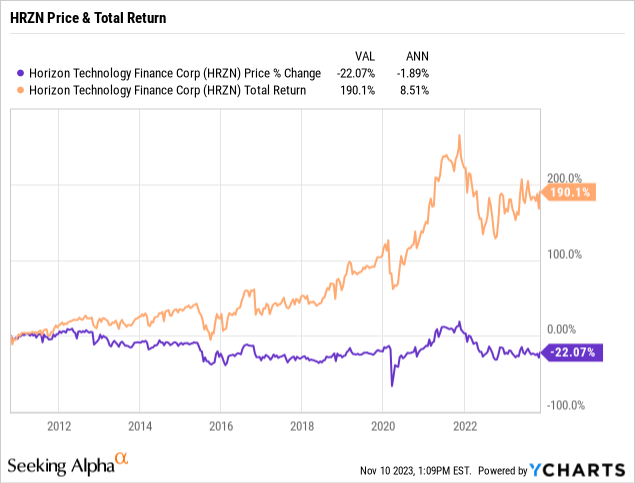

Since inception in 2011, HRZN has provided a price & total return of about -22% & 190% or -1.89% & 8.51% average annualized return respectively. Even with an average inflation rate of 2.65%, I believe a 6% annualized real return reflects a great income investment, especially in a stock/sector which traditionally has a low correlation, 0.59 in HRZN’s case, to the broader market.

Why I Continue The DRIP

- Dividends

- Earnings Trends

- Sustainable Income Investment

Dividends

HRZN has maintained a stable dividend profile with a 4 year average dividend yield of 9.89% and 5 year yield on cost of 11.07%. It’s generally maintained around this level for 10+ years. Dividend safety and sustainability are important to me and for a BDC like HRZN, I like to calculate their dividend coverage ratio to verify, by taking the quarterly or yearly Net Investment Income (NII) over the total dividends paid. Note, we can’t look at the calculated payout ratio as it’s not really representative of BDCs since they must payout 90% of their earnings to shareholders unlike a standard corporate stock which have no such requirement. Per their latest Q3 2023 Financial Results HRZN had a NII of $17.4M and paid out $10.991M in dividends giving a dividend coverage ratio of about 1.58. I actually prefer to flip the formula to calculate an equivalent “payout ratio” which is about 63% in this case. Either way you look at it, this indicates healthy dividend coverage, as the company can handily pay the dividend almost two times over, giving room for investment into new opportunities and leverage to manage inherent business model risks.

Over the years, HRZN’s healthy financials can also be reflected through their relatively recent $0.01 dividend increase from $0.10/share to $0.11/share and special dividend they’ve issued for 4 years in a row of $0.05/share. This special dividend is a nice 3.75% bonus for us investors. The $0.01 increase may not sound like much, but it is in fact a 10% increase to the distribution, which is timely as we cool off from a period of significantly higher than average inflation rates the last few years.

Earnings Trends

| Metric | Q3 2022 | Q3 2023 |

|---|---|---|

| Total Investment Portfolio | $634M | $729M |

| Net Investment Income (NII) | $11.1M | $17.4M |

| Debt Portfolio Yield | 15.9% | 17.1% |

There are several positive earnings trends from the financial results of HRZN for the third quarter of 2023 which catch my eye. The total investment portfolio grew to $729.1 million as of September 30, 2023, which represents a 15% increase year-over-year. With this increased portfolio growth, NII was reported to be $17.4M or $0.53/share which is a significant increase compared to the same period in the previous year when NII was $11.1 million or $0.43/share. This increase can be attributed in part to their debt portfolio yield increasing to 17.1% for the quarter, up from 15.9% the same period in the previous year.

The growth in both the portfolio size and NII indicates that the company is successfully expanding its investments, potentially leading to a higher Net Asset Value (NAV) and dividends & stability in the future, for now. This would also indicate their operation has benefited from the higher interest rate environment insofar. Overall, these positive trends suggest that HRZN had a successful quarter in terms expanding its portfolio, generating income, and maintaining a favorable yield on its debt investments.

Sustainability Backtest

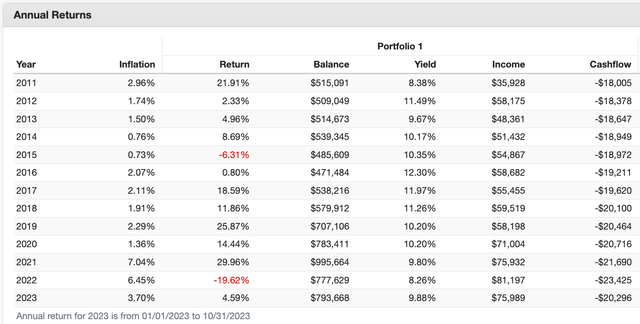

As always with my dividend and income investment selections, I like to do a backtest to check for sustainability using my core expenses: food, property taxes, insurance premiums, energy, water, internet, etc. which are about $2000/month today or $1462 in 2011 dollars. I base the monthly income number off the 4% rule benchmark, so $438k would have been required to live off of in 2011.

4% SWR Core Expenses Scenario: HRZN Performance Summary 2011-2023 (Portfolio Visualizer)

4% SWR Core Expenses Scenario: HRZN Annual Returns 2011-2023 (Portfolio Visualizer)

Good news, it passes my test: with an inflation adjusted CAGR of 2% and ever growing income stream. It’s also important to point out for those less experienced investing in BDCs (or REITs) that the market correlation with HRZN is only 0.59, which indicates the stock is not heavily correlated with the S&P500. This characteristic supports several positive trends and observations of HRZN, such as lower volatility, preservation of capital, and consistent dividend payouts.

Risk Analysis

Despite a lower beta supporting less systemic market risk, there are a few risks HRZN exposes investors to. Inherent to their fundamental business model, like many BDCs: they invest in debt and equity securities. This exposes the investment to pure credit risk, where their portfolio companies may not meet their debt obligations or go bankrupt. These scenarios would ultimately affect NAV and dividend payouts. HRZN gives guidance to its credit risk in the Q3 2023 report, which is slightly better than the standard risk rating system

As of September 30, 2023, June 30, 2023 and December 31, 2022, Horizon’s loan portfolio had a weighted average credit rating of 3.1, with 4 being the highest credit quality rating and 3 being the rating for a standard level of risk. A rating of 2 represents an increased level of risk and, while no loss is currently anticipated for a 2-rated loan, there is potential for future loss of principal. A rating of 1 represents deteriorating credit quality and high degree of risk of loss of principal.

In addition to credit risk, changes in interest rates, like the rising rates we’ve experienced the last year, can imply changes to both the underlying companies being invested in and the NAV of the stock. Of note, HRZN like other BDCs and REITs sell shares to raise capital for investments, especially during a high interest rate environment. The real risk here is an interaction between diluting shares to raise capital in order to loan money to companies, which decreases the NAV temporarily and now the companies need to be able to pay back the loans, which most of the income gets passed on to investors, which is all subject to credit risk. So, both these interacting events if gone well, keeps the NAV and dividends stable and growing but if the results go the wrong way, now we have a de-valued NAV and less income to distribute, which in turn raising more money for another round can either spook investors and further de-value the NAV. Thus, it’s critical BDC’s like HRZN shrewdly manage their portfolio to prevent this kind of situation from unfolding.

Forward Looking Sentiment

Looking ahead, I remain optimistic in my investment in HRZN. The company has demonstrated responsible management, good returns, and stable dividends I can ultimately count on to pay the bills and supplement my lifestyle. With the low market correlation and unique BDC play, I’ve owned HRZN for a long time and am happy with its returns and resilience throughout the last decade. In the coming years I would say consistent dividend growth and more price appreciation, at least maintained in positive territory, would drive me to dig in more heavily, but on the Horizon I’m content to continue reinvesting my shares, for now.